Future Preference

Merkle Manufactory, the company that stewards the Farcaster protocol and develops the Farcaster app has decided to pivot away from decentralized social media, choosing to build a crypto wallet instead (more here).

Inevitably, the feed is an onslaught of tokens and tickers, with a slew of scumbags seeking exit liquidity. It's Boiler Room brought forward to 2025, but without the ability to close.

I left Farcaster at the beginning of the year, but upon returning recently I found myself experimenting with Bracky, a sports betting prediction mini-app.

To be clear, I’d never gambled predicted on sports until using this mini-app.

It’s a great UI. Smooth digital interface.

But why am I using a protocol and application that encourages me to gamble participate in financialized prediction markets?

It’s not unique to Farcaster.

If anything, they’re five years behind the times.

During the pandemic (July 2020), I sent a newsletter to clients and friends active in private markets:

Lately, I’ve been thinking about the tokenization of assets.

I highlighted this trend in a previous newsletter [see Otis from September 2019], but the explosion of day traders in the U.S. stock market has me thinking about it in a new way.

You see, I have been bullish about what the digitization and securitization of non-traditional assets might mean for creatives globally, and EM in general — think of the possibilities for inclusive wealth creation in capital-light, culture-rich verticals and markets.

But I hadn’t considered how it impacts the psychology of investing.

Take a look at the Cash App, for example (disclosure: position in Square). The Cash App is but one example of technology democratizing access to financial markets.

In the Cash App, users can frictionlessly transfer money and trade stocks or bitcoin. In addition, users can purchase fractions of shares that they may not be able to afford otherwise (e.g., Apple, Mastercard).

The insight on investor psychology comes from the user interface and how it gamifies the process of ‘investing’.

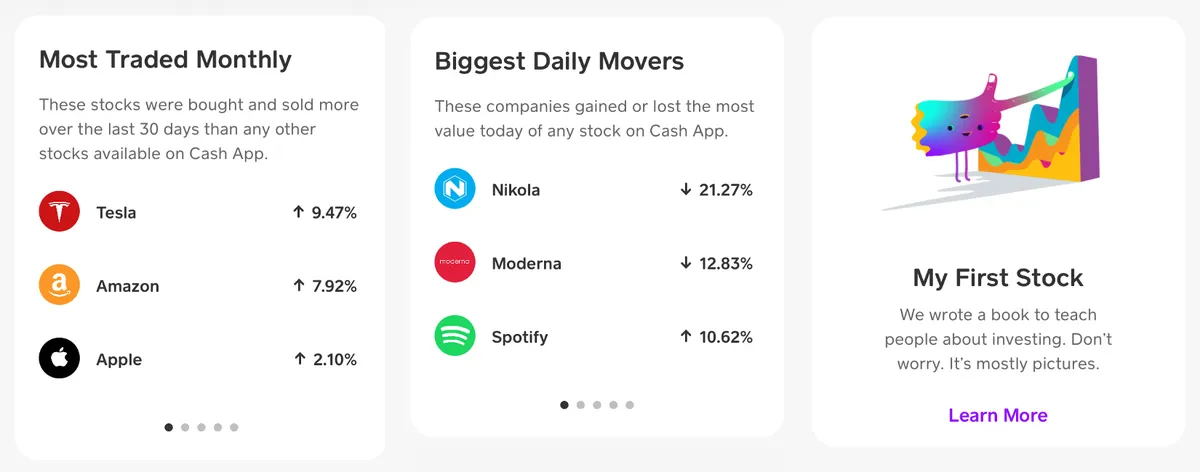

Take a look:

The logos of the most-traded and biggest-daily movers are presented like pennants at a horse race, highlighting two of the speculator’s best frenemies: volume and volatility.

There’s even a digital (picture) book to teach users about investing.

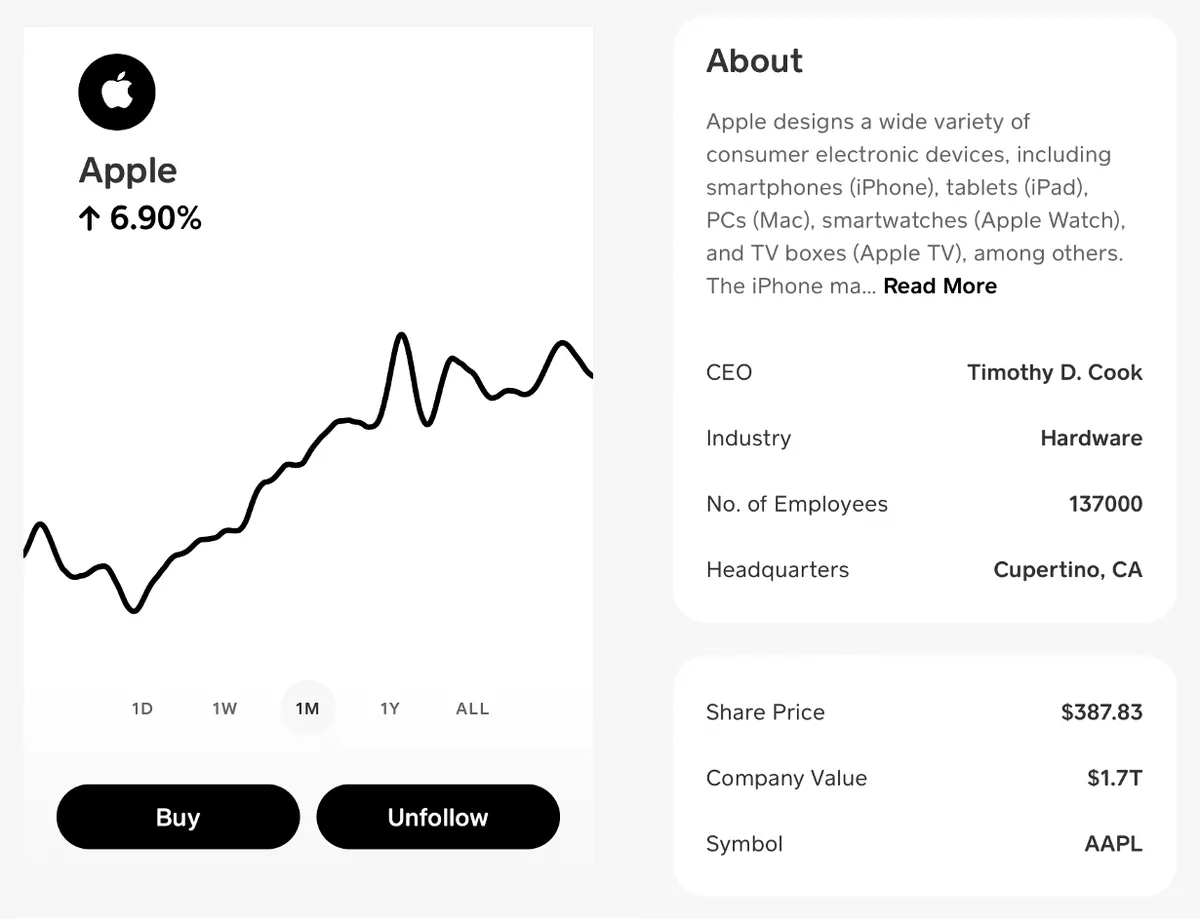

When you click on a company — say, Apple (no position) — the historical share price performance is presented with a soft, rounded line, evoking a languorous drive through the Tuscan hills.

There’s a brief snippet about what the company does, and three data points: number of employees, share price, and company value (market cap).

There are no fundamentals that traditional investors might wish to know, such as revenues or earnings, to say nothing of operational or financial performance metrics.

The share is the thing. Not the business.

The logo. Not the cash flow.

When I talk to day traders about the stocks they’re playing, they talk about shares like my friends and I yammered about baseball cards on the playground.

Back then, we’d reference an issue of Beckett to ascertain a card’s dollar value. Nevertheless, there was an emergent consensus on the cards that had value and those that did not — quality players, quality cardstock.

If there was a disagreement over a card’s value, the players’ stats were displayed on the back, enabling a fundamental comparison of their skills.

But I find that with day traders, the market value is irrelevant. What matters are movement and momentum.

“What does the company do? How does it make money? Is it profitable?” I ask.

🤷 “It’s up 30%.”

Look.

I speculate.

I own tokens, be they fungible or non-.

But there are two plagues of the ZIRP world: the elevation of expected value over expected utility, and the collapse in time preference.

In brief, the notion of expected value (EV) is summing the multiples of the probabilities and the payouts of an outcome. It’s basically gambling that you’ll win if you have enough cash to stay at the table for the law of averages to land.1

The best illustration of this phenomenon is Sam Bankman-Fried, whose purported belief in Effective Altruism prompted him to make positive-EV bets until he blew up FTX and much else besides. See, for example, Going Infinite.

It doesn’t have to be so dramatic. Much of venture capital runs on EV. Spray the cash around and one winner will make the portfolio.

Success is a byproduct of statistics, not a determinate belief in what should be built, why, and for whom.

On the collapse in time preference, when I wrote an op-ed piece for the WSJ ~15 years ago, the average holding period for stocks had declined to one year. A Google search suggests it’s now less than six months (Reuters reported it was less than 5 months in 2020).

The shitcoins being touted on Farcaster take the trading velocity to a whole new level (though with exponentially lower volumes than one would see on pump.fun/Solana—a played-out token launcher).

At bottom, the nexus of prioritizing EV and collapsing time preference is nihilism. It’s strip-mining attention and connections today, not building technology or value that compounds.

It’s rotten. Antithetical to where I want to spend my time.

— _

Most people in crypto don't have the money to avoid gambler's ruin.↩